How to Get Approved for a Credit Card Easily is one of the most common financial questions among first-time applicants, young professionals, students, freelancers, and individuals looking to build or rebuild their credit profile. In today’s competitive banking environment, credit card approval depends on far more than simply submitting an application. Banks analyze your credit behavior, income stability, debt obligations, repayment history, and overall financial responsibility before making a lending decision.

Understanding how lenders evaluate applicants can dramatically improve your approval chances. This complete guide explains the exact strategies, financial factors, approval requirements, and expert tips that can help you qualify for a credit card faster in 2026.

Table of Contents

🏦 Why How to Get Approved for a Credit Card Easily Depends on Bank Approval Factors

Before issuing a line of credit, banks evaluate one simple but critical question:

“Can this applicant borrow responsibly and repay consistently?”

Everything inside your application is analyzed to answer that question.

🔍 Key Financial Signals Banks Review

✅ Payment History:

Your payment history is often the strongest predictor of future repayment behavior.

Banks carefully review your previous borrowing patterns to understand whether you consistently meet financial obligations. A strong payment record demonstrates reliability, financial discipline, and lower lending risk.

A positive payment history may include on-time payments for loans, utility accounts, financing agreements, and previous credit accounts. Even one missed payment can temporarily reduce your approval odds because lenders view recent delinquencies as warning signs.

Consistently paying bills before due dates builds trust with lenders and improves your long-term financial profile.

✅ Income Stability:

Banks care less about how much you earn and more about how consistently you earn it.

A steady income suggests that you have predictable cash flow available to handle monthly repayments. Applicants with long-term employment, stable salary deposits, or documented self-employment income usually appear less risky.

Income sources may include:

✔ Full-time employment

✔ Part-time work

✔ Freelance contracts

✔ Business revenue

✔ Rental income

✔ Investment income

Lenders also review employment duration, employer reputation, and banking deposits to verify income consistency.

A moderate but stable income often performs better than a high but irregular income.

✅ Existing Debt Obligations:

Your current debt level directly affects your approval chances.

Banks evaluate whether your income is already heavily committed toward other financial obligations.

Common debt obligations include:

✔ Personal loans

✔ Auto financing

✔ Mortgage payments

✔ Existing credit cards

✔ Installment plans

If a large percentage of your monthly income is already allocated to debt payments, lenders may hesitate to extend additional credit.

Maintaining manageable debt levels improves your repayment profile and lender confidence.

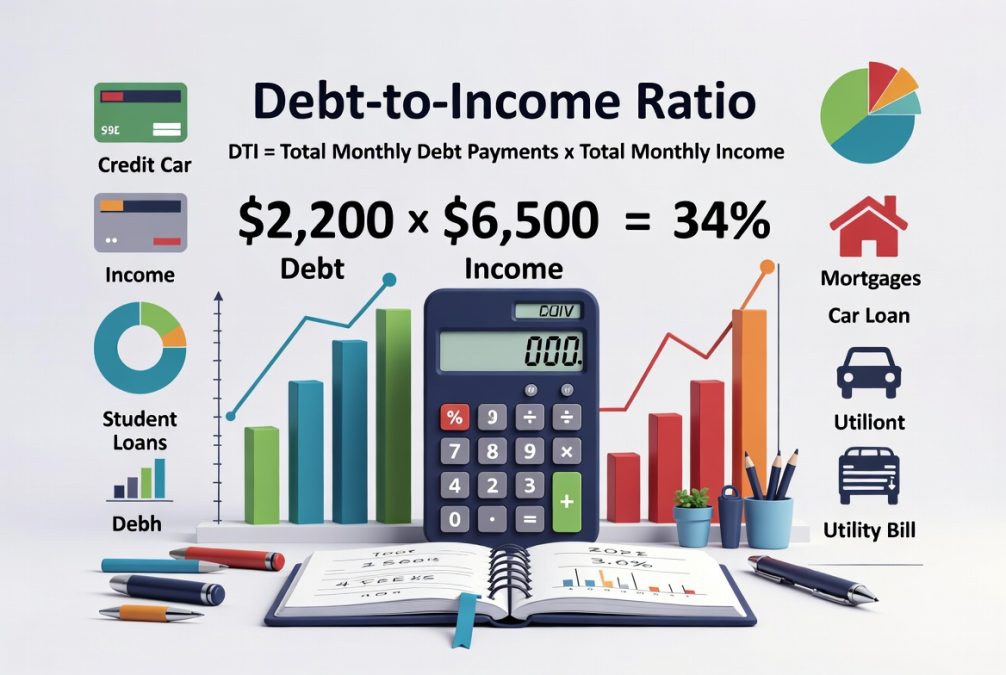

📊 How to Get Approved for a Credit Card Easily by Improving Your Debt-to-Income Ratio

Debt-to-Income Ratio (DTI) helps lenders measure repayment capacity.

DTI=Monthly IncomeMonthly Debt

💡 Why DTI Matters

✅ Lower DTI Builds Lender Confidence:

A low DTI indicates that you have enough disposable income after paying existing obligations.

When lenders see that your financial commitments consume only a small portion of your income, they are more confident in your ability to manage additional credit responsibly.

A healthy DTI also signals:

✔ Better budgeting habits

✔ Lower default risk

✔ Financial flexibility

✔ Strong repayment capacity

Many successful applicants maintain a DTI below 35%.

Reducing monthly debt before applying can significantly improve approval odds.

📈 How to Get Approved for a Credit Card Easily by Building a Strong Credit Score

Your credit score remains one of the most influential approval factors.

⭐ Why Credit Scores Matter

✅ Strong Scores Reduce Lending Risk:

Credit scores summarize your borrowing history into a numerical risk profile.

Higher scores typically indicate:

✔ On-time payments

✔ Low credit usage

✔ Responsible borrowing

✔ Long account history

✔ Minimal recent inquiries

A stronger score often unlocks:

✔ Higher approval odds

✔ Better credit limits

✔ Lower interest rates

✔ Premium rewards programs

Improving your score before applying can create measurable advantages.

🔍 How to Get Approved for a Credit Card Easily by Checking Your Credit Report

Many applicants get rejected because of inaccurate credit reporting.

⚠ Common Reporting Issues

✅ Incorrect Information Can Hurt Approval:

Your credit report may contain outdated or incorrect information that negatively impacts lender decisions.

Examples include:

✔ Duplicate accounts

✔ Incorrect balances

✔ Paid loans listed as active

✔ Fraudulent accounts

✔ Wrong late-payment entries

Reviewing your report before applying allows you to dispute errors and improve data accuracy.

Even small corrections can lead to stronger approval outcomes.

💳 How to Get Approved for a Credit Card Easily With Low Credit Utilization

Credit utilization measures how much of your available credit you currently use.

Utilization=Total Credit LimitUsed Credit

🎯 Why Utilization Matters

✅ Lower Utilization Signals Financial Control:

High utilization may suggest financial stress.

Low utilization shows lenders that you can access credit without becoming financially dependent on it.

Healthy utilization often indicates:

✔ Responsible spending

✔ Strong cash management

✔ Lower repayment risk

✔ Better budgeting discipline

Most financial experts recommend keeping utilization below 30%.

Many premium borrowers stay below 10%.

🕒 How to Get Approved for a Credit Card Easily by Applying at the Right Time

Timing can directly affect approval outcomes.

⏰ Best Times to Apply

✅ Strategic Timing Improves Approval Odds:

Submitting your application at the right financial moment can strengthen your profile.

Ideal situations include:

✔ After paying down balances

✔ After salary deposits

✔ After correcting report errors

✔ After avoiding new debt for several weeks

✔ After income increases

Strategic timing ensures lenders see your strongest financial snapshot.

🏛 How to Get Approved for a Credit Card Easily Through Banking Relationships

Existing banking relationships can improve lender trust.

🤝 Why Relationship Banking Works

✅ Familiar Customers Often Look Less Risky:

Banks already understand your deposit behavior, account balances, and financial habits.

Positive account history may include:

✔ Regular deposits

✔ Stable balances

✔ Long-term accounts

✔ No overdraft history

✔ Active account usage

Relationship banking can improve internal approval scoring.

🚫 How to Get Approved for a Credit Card Easily Without Multiple Applications

Too many applications can hurt your approval profile.

⚠ Why Multiple Applications Create Risk

✅ Hard Inquiries Affect Lender Perception:

Every formal application may generate a hard credit inquiry.

Multiple inquiries in a short period may signal:

✔ Financial stress

✔ Emergency borrowing

✔ High credit dependency

✔ Elevated repayment risk

Applying strategically preserves your credit strength.

🔒 How to Get Approved for a Credit Card Easily Using Secured Credit Cards

Secured cards can help applicants with limited or damaged credit.

🛡 Why Secured Cards Work

✅ They Help Build Financial Credibility:

Secured cards require a refundable deposit that reduces lender risk.

Benefits include:

✔ Credit history development

✔ On-time payment reporting

✔ Utilization improvement

✔ Account age development

✔ Future upgrade opportunities

Many successful borrowers begin with secured products.

📋 Final Checklist: How to Get Approved for a Credit Card Easily

Before applying, verify the following:

✅ Financial Preparation Checklist:

✔ Credit report reviewed

✔ Errors corrected

✔ Debt reduced

✔ Utilization optimized

✔ Income documented

✔ Banking records updated

✔ Application details verified

✔ Correct card tier selected

Proper preparation significantly improves approval odds.

🎯 Conclusion

Getting approved for a credit card is not about luck—it’s about financial positioning.

Banks reward applicants who demonstrate responsibility, stability, and lower repayment risk.

By improving your credit profile, reducing debt, maintaining income consistency, and applying strategically, you can dramatically increase your approval chances in 2026 and beyond.

The most successful applicants don’t apply first.

They prepare first—then apply with confidence.

❓ FAQs About How to Get Approved for a Credit Card Easily

1. What credit score do I need to get approved for a credit card?

Most lenders prefer scores above 670 for standard credit products, although beginner and secured cards may accept lower scores or limited credit history.

2. Can I get approved for a credit card with no credit history?

Yes. Many banks offer beginner-focused products such as secured credit cards and entry-level credit-building cards designed for first-time applicants.

3. How long should I wait after a rejected application?

Financial experts generally recommend waiting at least 30 to 90 days while improving your financial profile before reapplying.

4. Does income matter more than credit score?

Both matter. Stable income proves repayment ability, while credit score reflects repayment history. Lenders typically evaluate both together.

5. Do multiple credit applications hurt my score?

Yes. Multiple hard inquiries within a short period may temporarily lower your credit score and reduce approval odds.

6. Is pre-qualification guaranteed approval?

No. Pre-qualification indicates potential eligibility but final approval still depends on full underwriting review.

7. What is the ideal credit utilization ratio?

Most lenders prefer utilization below 30%, while below 10% is often considered excellent.

So, I ended up here somehow, not really sure how, even though I almost skipped it. I didn’t expect it to be this helpful without making it overly complicated. I didn’t expect to stay this long.

That’s honestly awesome to hear! I’m glad it turned out useful and easy to follow. Hope to see you around more often!