How to Use a Credit Card Safely (Beginner Tips for Smart Financial Control)

Introduction: Why Credit Card Safety Matters More Than Ever

How to use a credit card safely is one of the most important financial skills every beginner must learn in today’s digital economy. In the United States and across Europe, credit cards are widely used for daily purchases, online shopping, and travel. However, without proper knowledge and discipline, they can quickly lead to debt and financial stress.

However, for beginners, credit cards can quickly become a source of stress if not used responsibly. High interest rates, hidden fees, and overspending habits can turn a helpful tool into a financial burden.

This guide is designed to help you understand, manage, and safely use your credit card while building long-term financial stability.

🧾 What Is a Credit Card & How It Works

A credit card allows you to borrow money from a bank within a predefined limit. You can use it for purchases and repay the borrowed amount later, either in full or partially.

🔑 Key Components of a Credit Card:

- 💳 Credit Limit

- 📅 Billing Cycle

- ⏳ Due Date

- 📉 Interest Rate (APR)

- 💵 Minimum Payment

Understanding these basics is essential before applying any safety strategy.

🛡️ 1. 💰 Treat Your Credit Card Like Cash

- 💡 Explanation:

Using a credit card should never feel like accessing free money. Instead, you should treat every transaction as if you are paying directly from your bank account. This mindset helps prevent overspending and builds financial discipline over time. When you rely on actual available funds rather than future income, you naturally control unnecessary purchases. Many beginners fall into the trap of spending beyond their means because credit feels invisible compared to cash. By aligning your spending with your real income, you avoid debt accumulation and reduce financial stress. This habit also ensures you always have enough funds to pay your full balance on time. Over time, this approach strengthens your budgeting skills and improves your overall financial health.

🛡️ 2. 📆 Always Pay Your Balance in Full

- 💡 Explanation:

Paying your full credit card balance every month is the most effective way to avoid interest charges. Credit cards often come with high interest rates, especially in the US and European markets, which can quickly increase your total debt. When you pay in full, you benefit from the interest-free grace period offered by most issuers. This means you essentially use the bank’s money without paying extra. On the other hand, carrying a balance leads to compounding interest, making even small purchases expensive over time. Consistently paying in full also boosts your credit score and shows lenders that you are financially responsible. It builds trust and can help you qualify for better financial products in the future.

🛡️ 3. ⏰ Never Miss a Payment

- 💡 Explanation:

Missing a credit card payment can have serious consequences beyond just a late fee. It can negatively impact your credit score, which plays a crucial role in financial systems across the US and Europe. A lower credit score can affect your ability to get loans, rent apartments, or even secure certain jobs. Additionally, repeated late payments may result in higher interest rates or account restrictions. Setting up automatic payments or reminders ensures you never miss a due date. Consistency is key to maintaining a strong credit profile. Even one missed payment can stay on your credit report for years, so building a habit of timely payments is essential for long-term financial success.

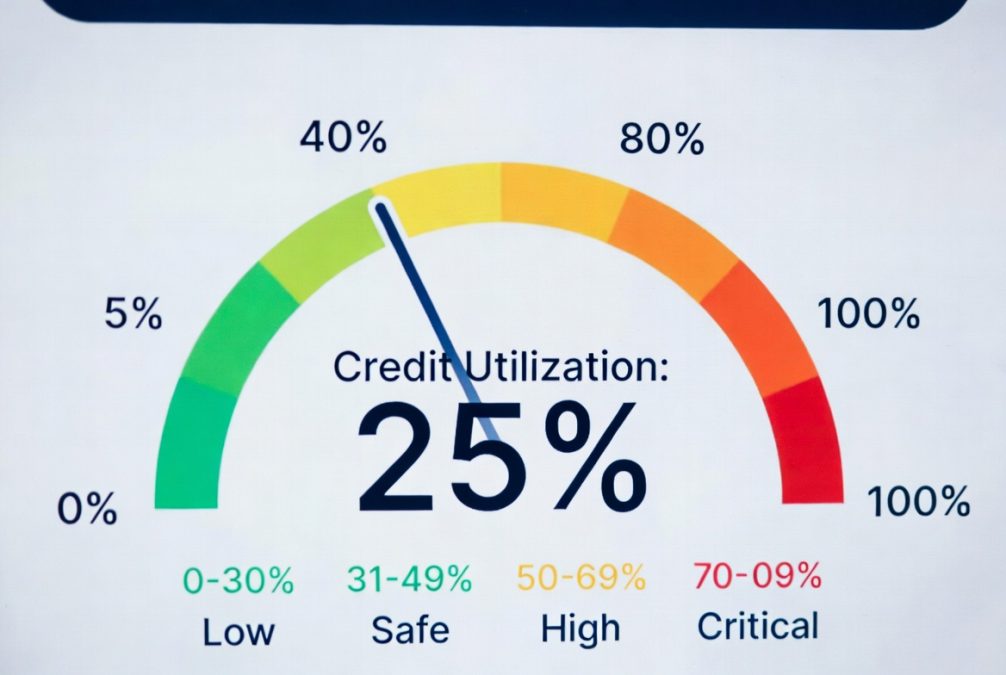

🛡️ 4. 📊 Keep Your Credit Utilization Low

- 💡 Explanation:

Credit utilization refers to how much of your available credit you are using. Experts recommend keeping it below 30% of your total limit. For example, if your limit is $1,000, try not to exceed $300. High utilization signals financial risk to lenders and can lower your credit score. Keeping it low demonstrates that you are not overly dependent on borrowed money. It also gives you a safety buffer in case of emergencies. Regularly monitoring your usage helps maintain a healthy balance between spending and available credit. Over time, low utilization contributes to a stronger credit profile and better financial opportunities.

🛡️ 5. 🛍️ Avoid Impulse Spending

- 💡 Explanation:

Impulse spending is one of the biggest dangers of credit card usage. The ease of swiping or clicking “buy now” can lead to unnecessary purchases that quickly add up. Emotional buying, especially during sales or stress, often results in regret and financial strain. Implementing a 24-hour rule before making non-essential purchases can significantly reduce impulsive decisions. This pause allows you to evaluate whether the purchase is truly needed. Developing mindful spending habits helps you stay within your budget and avoid debt. Over time, this discipline leads to better financial control and smarter decision-making.

🛡️ 6. 📱 Track Every Transaction

- 💡 Explanation:

Monitoring your credit card activity is essential for maintaining control over your finances. Many banks offer mobile apps that provide real-time transaction updates. By regularly reviewing your spending, you can identify patterns and adjust your budget accordingly. This practice also helps detect unauthorized transactions early, reducing the risk of fraud. Ignoring your spending can lead to surprises at the end of the billing cycle. Staying informed ensures you are always aware of your financial position. It also encourages accountability and helps you make better financial choices.

🛡️ 7. 🔐 Protect Your Card Information

- 💡 Explanation:

Security is a critical aspect of credit card usage, especially with the rise of online transactions. Protecting your card details from fraud and theft should be a top priority. Avoid sharing your information on unsecured websites or public networks. Always check for secure connections (HTTPS) when making online payments. Enabling transaction alerts adds an extra layer of protection. If you notice suspicious activity, report it immediately to your bank. Quick action can prevent further and protect your funds. Staying vigilant ensures your financial data remains safe in an increasingly digital world.

🛡️ 8. 🌐 Be Careful with Online Shopping

- 💡 Explanation:

Online shopping offers convenience but also comes with risks. Fake websites, phishing scams, and data breaches are common threats. Always shop from reputable platforms and avoid deals that seem too good to be true. Using virtual cards or secure payment methods can reduce risk. Additionally, avoid saving your card details on multiple websites. Taking these precautions helps protect your financial information. As e-commerce continues to grow in the US and Europe, being cautious online is more important than ever.

🛡️ 9. 📉 Understand Interest Rates (APR)

- 💡 Explanation:

Interest rates determine how much extra you pay if you carry a balance. Credit card APRs are typically higher than other forms of credit, making them expensive if misused. Understanding how interest is calculated helps you make informed decisions. Even small unpaid balances can grow significantly over time due to compounding. By paying your balance in full, you can avoid these charges entirely. Being aware of your card’s APR allows you to plan your finances better and avoid unnecessary costs.

🛡️ 10. 🚫 Avoid Minimum Payments Trap

- 💡 Explanation:

Paying only the minimum amount may seem convenient, but it keeps you in debt longer. Most of your payment goes toward interest rather than the principal balance. This means it can take years to pay off even a small amount. Over time, you end up paying much more than the original purchase. Always aim to pay more than the minimum, ideally the full balance. This approach reduces interest and helps you stay debt-free.

🛡️ 11. 🏦 Choose the Right Credit Card

- 💡 Explanation:

Selecting the right credit card is crucial for beginners. Look for features like low interest rates, no annual fees, and user-friendly mobile apps. Some cards offer rewards such as cashback or travel points, which can add value if used responsibly. However, avoid choosing a card based solely on rewards. Your primary focus should be ease of management and affordability. A well-chosen card simplifies your financial journey and supports responsible usage.

🏁 Conclusion: Build Smart Credit Habits Today

Using a credit card safely is not about avoiding it—it’s about using it wisely. By following these beginner-friendly tips, you can enjoy the benefits of credit cards without falling into debt.

Developing disciplined habits early will help you:

- Build a strong credit score

- Avoid unnecessary interest

- Maintain financial stability

Remember, your credit card should work for you—not against you.

❓ FAQs

❓ What is the safest way to use a credit card?

The safest way is to spend within your means, pay your balance in full every month, and never miss a payment.

❓ How can beginners avoid credit card debt?

Beginners should track spending, avoid impulse purchases, and always pay more than the minimum balance.

❓ What is a good credit utilization ratio?

A good ratio is below 30% of your total credit limit.

❓ Does using a credit card build credit score?

Yes, responsible usage like on-time payments and low balances improves your credit score.

❓ Is it bad to pay only the minimum amount?

Yes, it increases interest and prolongs debt repayment.