Top Financial Mistakes to Avoid in Your 20s and 30s (Complete Guide for Long-Term Wealth)

📌 Introduction

Your 20s and 30s are the most critical decades for building financial stability and long-term wealth. The habits you form, the decisions you make, and the mistakes you avoid during these years can define your financial future.

Many people in the United States and Europe struggle not because they don’t earn enough—but because they make avoidable financial mistakes early in life. These mistakes often seem small at first but can compound into serious financial stress later.

This comprehensive guide will walk you through the most common financial mistakes in your 20s and 30s, explain why they matter, and show you how to avoid them using proven, practical strategies.

🚫 1. Living Beyond Your Means

🔹 What This Means

Spending more money than you earn, often driven by lifestyle inflation and social pressure.

🔸 Key Risks:

- 💳 Overspending habits:

When you consistently spend more than you earn, your financial stability weakens over time. This behavior often starts with small indulgences—frequent dining out, upgrading gadgets, or luxury subscriptions—but gradually becomes a habit. Overspending reduces your ability to save and forces dependence on credit, which can lead to long-term debt cycles. Over time, this creates financial stress and limits your ability to invest or prepare for emergencies. - 📉 No savings growth:

Without controlling expenses, your savings remain stagnant or nonexistent. Even with a good income, failing to save regularly means you miss opportunities to build wealth. Savings are the foundation of financial security, helping you manage emergencies, invest, and plan for future goals like homeownership or retirement. A lack of savings leaves you vulnerable to unexpected financial shocks. - 🔄 Lifestyle inflation trap:

As your income increases, your expenses rise at the same pace—or faster. This prevents wealth accumulation because you never truly “get ahead.” Instead of improving your financial position, you remain stuck in a cycle of earning and spending. Over time, this habit delays financial independence and reduces your ability to build long-term assets.

💳 2. Misusing Credit Cards

🔹 What This Means

Using credit irresponsibly, leading to high-interest debt.

🔸 Key Risks:

- 📈 High-interest accumulation:

Credit cards often carry high interest rates, especially in the U.S. and Europe. When balances are not paid in full, interest compounds quickly, turning small purchases into large debts. Over time, this can significantly increase the total amount you owe, making it harder to achieve financial stability. - ⚠️ Minimum payment trap:

Paying only the minimum due each month may seem manageable, but it extends your repayment period and increases interest costs. This approach can keep you in debt for years, even for relatively small balances. It creates a false sense of affordability while quietly draining your finances. - 📉 Credit score damage:

High credit utilization and late payments negatively impact your credit score. A poor credit score can affect your ability to secure loans, rent apartments, or even get favorable insurance rates. Maintaining good credit is essential for financial flexibility and future opportunities.

🏦 3. Not Building an Emergency Fund

🔹 What This Means

Failing to set aside money for unexpected expenses.

🔸 Key Risks:

- 🚨 Financial vulnerability:

Without an emergency fund, unexpected expenses like medical bills or car repairs can disrupt your entire financial plan. You may be forced to rely on high-interest debt or liquidate investments prematurely, both of which can harm your financial future. - 💸 Increased debt reliance:

In the absence of savings, many people turn to credit cards or personal loans during emergencies. This can quickly lead to a cycle of debt that becomes difficult to escape. Emergency funds act as a financial buffer, reducing reliance on borrowed money. - 🧠 Mental stress and uncertainty:

Financial insecurity often leads to stress and anxiety. Knowing you have savings set aside provides peace of mind and allows you to handle unexpected situations with confidence. It also helps you make better financial decisions without panic.

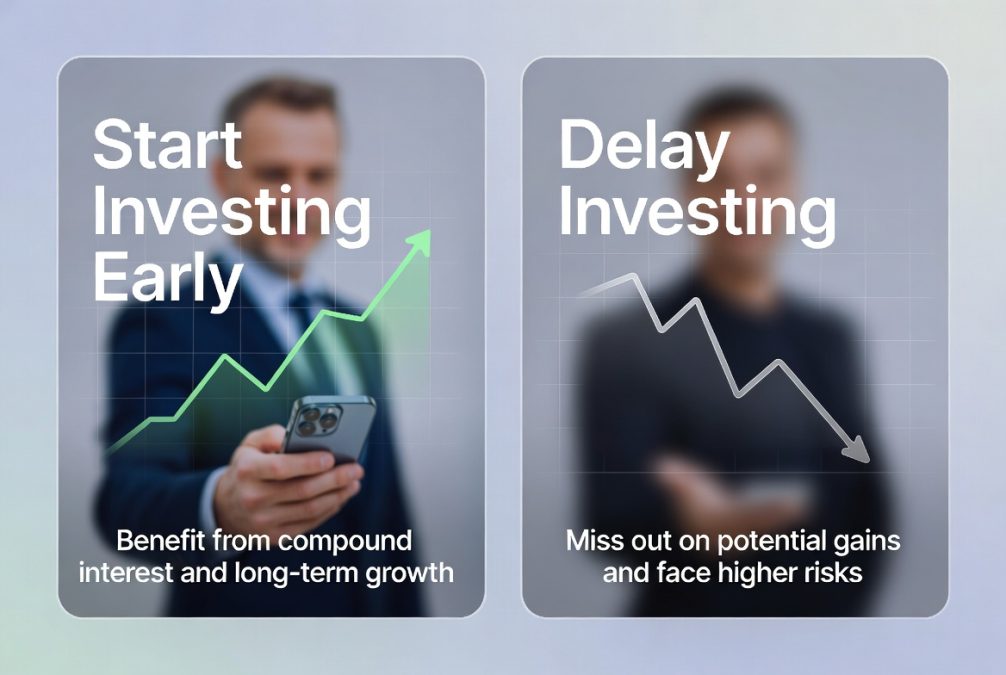

📉 4. Delaying Investing Too Long

🔹 What This Means

Waiting years before starting to invest.

🔸 Key Risks:

- ⏳ Lost compound growth:

Time is the most powerful factor in investing. The earlier you start, the more your money grows through compounding. Delaying even a few years can significantly reduce your total returns over time, making it harder to build wealth. - 📊 Missed market opportunities:

Financial markets grow over time despite short-term fluctuations. Waiting for the “perfect time” often results in missed opportunities. Consistent investing, even in small amounts, is more effective than trying to time the market. - 🏖️ Delayed retirement goals:

Starting late means you need to invest much larger amounts later to achieve the same retirement goals. Early investing reduces pressure and allows for a more comfortable and flexible financial future.

🧾 5. Ignoring a Budget

🔹 What This Means

Not tracking income and expenses.

🔸 Key Risks:

- 🔍 Lack of financial awareness:

Without a budget, you don’t fully understand where your money goes. This lack of visibility makes it difficult to identify unnecessary expenses or areas for improvement. Financial awareness is the first step toward control. - 💰 Uncontrolled spending:

When spending is not tracked, it often exceeds expectations. Small, frequent expenses add up quickly and can derail your financial plans. Budgeting helps you set limits and prioritize essential expenses. - 📉 Difficulty achieving goals:

Without a clear plan, it becomes harder to save for specific goals like travel, homeownership, or retirement. A budget aligns your spending with your priorities, making goal achievement more realistic.

🛍️ 6. Spending to Impress Others

🔹 What This Means

Making financial decisions based on social pressure.

🔸 Key Risks:

- 🎭 False lifestyle image:

Many people spend money to appear successful rather than actually becoming financially stable. This often involves luxury purchases that provide temporary satisfaction but long-term financial strain. - 💳 Increased debt burden:

Trying to keep up with others can lead to unnecessary borrowing. This creates financial obligations that may not align with your income, leading to stress and reduced financial flexibility. - 🧠 Emotional dissatisfaction:

Spending for validation rarely brings lasting happiness. Instead, it often results in regret and frustration. True financial confidence comes from stability, not appearances.

🚗 7. Buying an Expensive Car Too Early

🔹 What This Means

Purchasing a high-cost vehicle before achieving financial stability.

🔸 Key Risks:

- 📉 Rapid depreciation:

Cars lose value quickly, especially in the first few years. This means you are paying for an asset that decreases in value over time, unlike investments that grow. - 💸 High ownership costs:

Beyond the purchase price, cars come with ongoing expenses such as insurance, maintenance, fuel, and taxes. These costs can significantly impact your monthly budget. - 🔒 Reduced financial flexibility:

High car payments limit your ability to save, invest, or pursue other financial goals. Choosing a more affordable vehicle can free up resources for wealth-building activities.

📈 8. Not Setting Financial Goals

🔹 What This Means

Living without clear financial objectives.

🔸 Key Risks:

- 🎯 Lack of direction:

Without goals, your financial decisions may lack purpose. This can lead to inconsistent saving and spending habits, making it harder to achieve meaningful progress. - 🕒 Wasted time and resources:

Time is a valuable financial asset. Without clear goals, you may miss opportunities to invest or save effectively, delaying your financial growth. - 📉 Low motivation:

Goals provide motivation and discipline. They help you stay focused and committed to your financial plan, even during challenging times.

📊 Conclusion

Avoiding financial mistakes in your 20s and 30s is one of the smartest decisions you can make. These years provide a powerful opportunity to build habits that lead to long-term financial success.

By controlling spending, managing debt, investing early, and setting clear goals, you can create a strong financial foundation that supports your future lifestyle.

Remember, financial success is not about how much you earn—it’s about how wisely you manage what you have.

❓ FAQs

❓ What are the biggest financial mistakes in your 20s?

The most common mistakes include overspending, not saving, avoiding investing, and misusing credit cards. These habits can delay financial growth and create long-term debt.

❓ How much should I save in my 20s and 30s?

Experts recommend saving at least 20% of your income. Start small if needed, but focus on consistency and gradual increases.

❓ Is it too late to start investing in your 30s?

No, it’s never too late. While starting earlier is better, investing in your 30s can still lead to significant financial growth over time.

❓ Why is budgeting important for young adults?

Budgeting helps track spending, control expenses, and ensure that financial goals are met. It provides clarity and financial discipline.

❓ How can I avoid debt in my 20s?

Avoid unnecessary borrowing, pay credit card balances in full, and live within your means. Focus on building savings and financial awareness.