💳 How Credit Cards Work – Simple Explanation for Beginners

Credit cards are one of the most essential financial tools in modern life, especially in the United States and Europe where digital payments dominate everyday transactions. Whether you are shopping online, booking travel, or handling emergency expenses, understanding how credit cards work is critical for managing your finances effectively.

👉 In simple terms:

A credit card allows you to borrow money from a bank and repay it later, either in full or over time with interest.

Table of Contents

📘 🧾 What is a Credit Card?

A credit card is a revolving line of credit provided by a financial institution. Unlike debit cards, which use your own money, credit cards let you spend the bank’s money within a set limit.

🔹 Key Concept:

You are borrowing money temporarily and agreeing to repay it under specific terms.

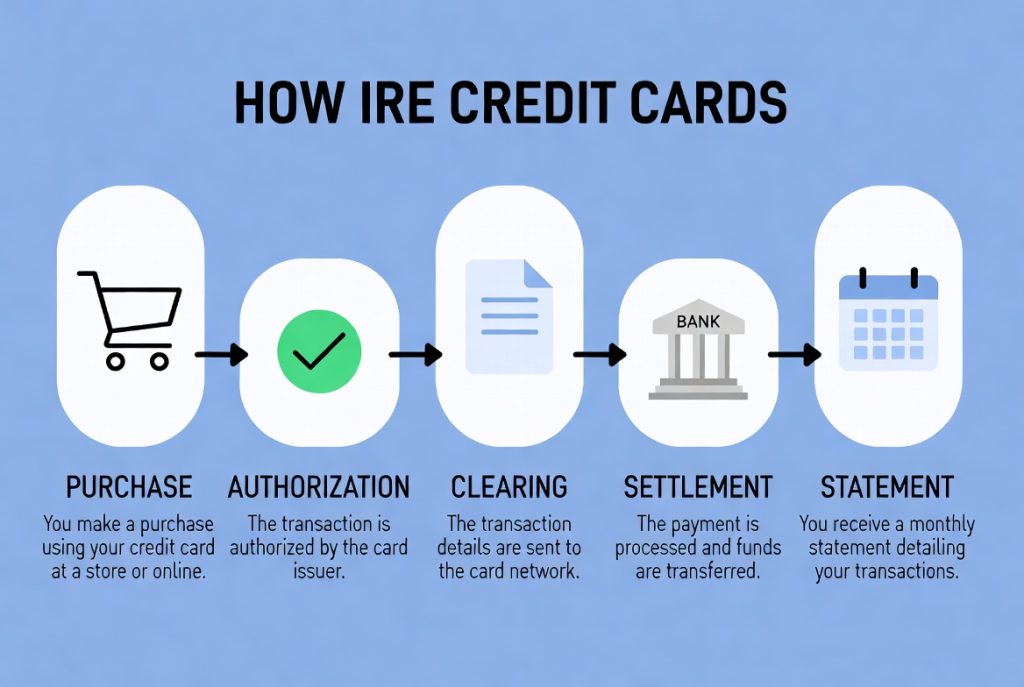

⚙️ 🔄 How Credit Cards Work (Step-by-Step)

Understanding the working process is essential for beginners:

🔸 Step 1: Purchase Transaction

When you swipe your card or enter details online, the issuing bank pays the merchant instantly.

🔸 Step 2: Transaction Recording

Each purchase is recorded in your account and contributes to your outstanding balance.

🔸 Step 3: Billing Cycle Completion

At the end of the billing cycle (usually 28–31 days), your statement is generated.

🔸 Step 4: Statement Generation

Your monthly statement includes total balance, minimum due, and payment due date.

🔸 Step 5: Payment Options

You can either pay the full amount or make a minimum payment, depending on your financial situation.

📅 ⏳ Billing Cycle & Grace Period Explained

🔹 Billing Cycle:

The time period during which your transactions are recorded before a bill is generated.

🔹 Grace Period:

The interest-free period between statement generation and due date.

👉 Paying your full balance within this period helps you avoid interest completely.

💰 📊 Credit Limit & Utilization

🔹 Credit Limit:

The maximum amount you can borrow using your card.

🔹 Credit Utilization:

The percentage of your limit that you use.

👉 Keeping utilization below 30% is ideal for maintaining a strong credit profile.

📉 💵 Interest Rates (APR) Explained

APR (Annual Percentage Rate) is the cost of borrowing if you carry a balance.

👉 Important Insight:

Credit card APRs are significantly higher than personal loans, which makes timely repayment crucial.

⚠️ 💸 Credit Card Fees (Detailed Breakdown)

🔴 Annual Fee:

The yearly cost of owning certain premium credit cards:

Many cards in the U.S. and Europe charge annual fees in exchange for premium features such as travel rewards, lounge access, or cashback bonuses. While some beginner cards have no annual fee, premium cards can charge anywhere from $50 to $500 or more annually. It is important to evaluate whether the benefits outweigh the cost. For example, frequent travelers may find value in travel perks, while casual users might prefer no-fee options. Always read the terms before applying. Choosing the right card based on your lifestyle can save money in the long run. Annual fees are not inherently bad, but they should align with your spending habits and financial goals.

🔴 Late Payment Fee:

Penalty charged when you miss your due date:

Missing a payment deadline can result in significant late fees, often ranging from $25 to $40 depending on your provider. Beyond the fee itself, late payments can negatively impact your credit score, making it harder to get loans in the future. Payment history is one of the most important factors in credit scoring models. Even a single missed payment can stay on your report for years. To avoid this, set up automatic payments or reminders. Consistency is key when managing credit responsibly. Paying even the minimum amount on time is better than missing a payment entirely. Developing disciplined habits early can protect your financial reputation.

🔴 Over-limit Fee:

Charged when you exceed your credit limit:

Although less common today, some credit card providers still charge fees if you exceed your assigned credit limit. Going over your limit may also trigger a penalty APR, increasing your interest rate. This can make repayment more expensive over time. Additionally, high utilization can damage your credit score. It is always recommended to monitor your spending regularly through mobile banking apps. Setting alerts can help prevent accidental overspending. Staying within your limit shows lenders that you are financially responsible. Responsible usage leads to better credit opportunities in the future.

🔴 Cash Advance Fee:

Cost of withdrawing cash using your credit card:

Using a credit card to withdraw cash is one of the most expensive actions you can take. Cash advances usually come with higher interest rates and no grace period, meaning interest starts accumulating immediately. On top of that, there is often a transaction fee of 3%–5%. This makes it a very costly option compared to regular purchases. Financial experts strongly advise against using credit cards for cash withdrawals unless absolutely necessary. It should only be used in emergencies when no other option is available. Understanding this feature can help you avoid unnecessary debt.

🎁 🎯 Credit Card Rewards & Benefits

🟢 Cashback Rewards:

Earn a percentage back on your spending:

Cashback cards are popular in the U.S. and Europe because they offer direct financial returns on everyday purchases. Typically, users can earn between 1% and 5% cashback depending on the category, such as groceries, gas, or dining. This means you get a portion of your money back simply for using the card. Over time, these rewards can add up significantly. However, it is important not to overspend just to earn rewards. The key is to use the card for planned expenses. Cashback rewards are simple and easy to understand, making them ideal for beginners. Choosing the right cashback categories can maximize your savings.

🟢 Travel Rewards:

Points or miles for travel-related spending:

Travel credit cards are designed for frequent flyers and travelers. They allow users to earn airline miles or hotel points, which can be redeemed for flights, upgrades, or accommodations. Some cards also include perks like travel insurance, priority boarding, and airport lounge access. While these benefits are attractive, they often come with higher annual fees. It is important to calculate whether the rewards justify the cost. Strategic use of travel cards can significantly reduce travel expenses. Planning purchases around reward categories can maximize benefits. This feature is ideal for people who travel regularly for work or leisure.

🟢 Fraud Protection:

Security against unauthorized transactions:

Modern credit cards come with advanced security features that protect users from fraud. If an unauthorized transaction occurs, most issuers offer zero-liability protection, meaning you are not responsible for fraudulent charges. Real-time alerts, chip technology, and two-factor authentication add additional layers of security. This makes credit cards safer than cash or even debit cards in many cases. Monitoring your account regularly is still important. Quick reporting of suspicious activity ensures faster resolution. This feature provides peace of mind and enhances user confidence. Security is one of the strongest advantages of using credit cards.

📈 📊 Credit Score & Its Importance

Your credit score reflects your financial reliability. It plays a major role in loan approvals, mortgage rates, and even job applications in some regions.

👉 Key Factors:

- Payment history

- Credit utilization

- Length of credit history

A strong credit score opens doors to better financial opportunities.

⚠️ 🚫 Common Credit Card Mistakes (Avoid These)

🔻 Paying Only Minimum Amount:

Leads to long-term debt accumulation:

Paying only the minimum due might seem convenient, but it can trap you in a cycle of debt. Interest continues to accumulate on the remaining balance, making your total repayment much higher over time. What starts as a small balance can grow into a large financial burden. This is how many users fall into long-term credit card debt. Always aim to pay the full balance whenever possible. If not, pay more than the minimum to reduce interest. Understanding this mistake early can save you thousands of dollars. Responsible repayment is the foundation of financial stability.

🔻 Missing Payments:

Damages your credit score significantly:

Missing payments not only results in late fees but also harms your credit score. Since payment history is a major factor in credit scoring, consistent late payments can lower your score quickly. This can affect your ability to get loans, mortgages, or even rental approvals. Setting up autopay or reminders can help avoid this issue. Financial discipline is essential when managing credit cards. Even one missed payment can have long-term consequences. Staying organized ensures you maintain a positive financial profile.

✅ 🧠 Smart Credit Card Tips for Beginners

🟢 Pay Full Balance Always:

Avoid interest completely:

Paying your full balance each month is the best way to use a credit card. It allows you to enjoy all the benefits without paying any interest. This habit ensures that you stay debt-free while building a positive credit history. It also demonstrates financial responsibility to lenders. Over time, this can improve your credit score significantly. Treat your credit card like a debit card—only spend what you can afford to repay. This simple rule can prevent most financial problems. Discipline and consistency are key to success.

🟢 Keep Utilization Low:

Maintain a healthy credit profile:

Using less than 30% of your credit limit shows lenders that you are not overly dependent on credit. High utilization can signal financial stress and lower your credit score. Even if you pay your balance in full, high usage during the billing cycle can still impact your score. Spreading expenses across multiple cards or making early payments can help maintain low utilization. This strategy improves your overall creditworthiness. Managing utilization effectively is a smart financial move. It reflects strong money management skills.

📊 ⚖️ Credit Card vs Debit Card

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Funds | Borrowed Money | Your Own Money |

| Interest | Yes (if unpaid) | No |

| Rewards | Yes | Limited |

| Credit Score Impact | Yes | No |

📌 🧾 Conclusion

Credit cards are powerful financial tools when used responsibly. They provide convenience, security, and valuable rewards—but they also require discipline and awareness.

👉 Key Takeaway:

Use your credit card wisely, pay on time, and avoid unnecessary debt.

Mastering these basics will help you build a strong financial future.

❓ 📢 FAQs (SEO Optimized for Google, Bing, Baidu & Yandex)

❓ What is the best way to use a credit card?

The best way is to pay your full balance on time every month and keep your usage below 30% of your credit limit.

❓ Do credit cards charge interest every month?

No, interest is only charged if you carry a balance beyond the grace period.

❓ Can beginners get a credit card easily?

Yes, beginners can start with secured or student credit cards and build their credit history over time.

❓ What happens if I miss a credit card payment?

You may face late fees, higher interest rates, and a drop in your credit score.

❓ Are credit cards safe to use online?

Yes, credit cards offer strong fraud protection and are generally safer than debit cards for online transactions.

I simply couldn’t go away your web site prior to suggesting

that I extremely loved the standard info an individual provide on your guests?

Is gonna be again continuously to check up on new

posts

Thanks a lot for your support! I’m happy you liked the information, and I look forward to seeing you again on new posts.